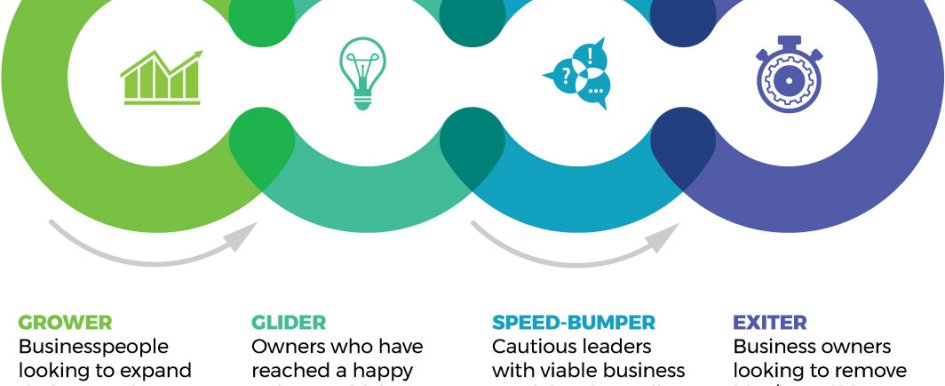

Just as we experience spring, summer, fall and winter each year, there are four main cycles for entrepreneurs as well. As a business owner, it is important to understand which cycle you are presently in, as it determines how you approach growth, helps pinpoint your most comfortable financial options and reveals your risk tolerance level. From start to finish of running a company, you will always either be growing, gliding, hitting a speed-bump or exiting.

Consider the case of John, a man in his early sixties, whose construction company has coasted along for years. Though at a much slower pace than 20 years ago, his business is growing steadily. John is financially set for life and wants to enjoy retirement by traveling with his wife and spending time with his grandchildren. There is no immediate hurry, but John is looking to cash out his company, which is now largely in the hands of his capable daughter. As you might guess, John is an exiter.

At a social function, John strikes up a conversation with husband-and-wife team Jason and Tara who run a fledgling construction company of their own and are not a direct competitor. Jason and Tara have just won a significant contract, and their products are receiving good reviews, but they need capital to meet their demands. These classic growers ask John for advice, figuring correctly that he has seen it all. An aggressive businessman all his life, John essentially tells Jason and Tara to be bold—the only way to successfully get through each individual entrepreneurial cycle.

1. Growers

A grower is the type of entrepreneur typically depicted in film, television, books and all other forms of media. These are the businesspeople looking to expand their operations, often rapidly. They generally have a healthy appetite for assuming risk and are loaded with self-confidence.

John tests Jason and Tara by asking them what they would do if they received a $1-million-gift. Would they invest all (or most) of that money directly into their business, or would they hold on to it, essentially saving it for a rainy day?

John is happy to hear that his newfound friends don’t hesitate before saying they are confident in their business and figure that investing the money would go a long way toward solving their growth issues. He tells them that since their business prospects are solid, there would be numerous financing options available for them, ranging from the tried-and-true Small Business Administration (SBA) loan, to the ancient practice of factoring, to every option in between.

While John is speaking, his audience grows, enthralled by the wisdom he’s imparting. One of the listeners is a long-time friend named Mary whose small chain of custom-framing stores is stable and profitable. She is a glider.

2. Gliders

Mary tells the group that she has reached a happy point at which she is making a solid amount of money, expects her business to remain sound and is in no hurry to wreck a good thing.

John has been somewhat of a mentor to Mary over the years and poses the same hypothetical $1-million-gift question he just asked Jason and Tara.

This leads Mary to waffle a bit. She first says she would place a significant chunk of that gift into mutual funds, which have with a smaller return, but are still available for use, if need be. After more thought, she decides that placing about 75 percent into her business would be best because she is already generating a higher return than a mutual fund would offer.

John approves, noting that keeping a business on an even keel is never a bad thing, especially for someone like Mary, who is beginning to consider retirement options. He also points out that since her business is doing well, there would be no shortage of palatable financial options available, if the need arose.

The conversation lurches in a different direction, however, when a frazzled-looking entrepreneur joins the discussion—Derek, the founder of an online sporting goods store. Derek’s business is growing at a double-digit rate, but he overestimated his market and is now stuck with a warehouse full of unsold goods. His bank wants to pull its line of credit and is demanding repayment. A textbook speed-bumper, Derek asks John what he should do.

3. Speed-Bumpers

John points out that a little rain falls on most people’s lives at some point, and entrepreneurs aren’t immune. Again, he brings up the hypothetical $1-million-gift. It doesn’t take long for Derek to respond that he would plunk most or the entire hypothetical money into his business. While some non-entrepreneurs might consider that foolish, Derek realizes that for any business to succeed, it requires the stomach for at least some risk, along with overriding confidence. By looking at the big picture, he realizes that—missteps aside—his company and business model are viable and will need some fine tuning.

John cautions that challenges might lie ahead because some financial options will be closed to Derek, and the options that will be open may carry a greater risk (or interest rate) and potentially even the surrendering of some equity. Having provided his sage advice to the others, the group of entrepreneurs questions John about his plans.

4. Exiters

John replies that even the most-fervent entrepreneur will walk away at some point. The reason doesn’t really matter. The group then turns the table on John and asks him what he would do with the $1-million-gift. Not surprisingly, he says he would invest half of it in mutual funds and put the rest back into the business, noting that it would help his successor daughter.

John points out that succession planning is important, but too many businesses either overlook it or give it brief thought. After all, who wants to be thinking about the distant future when the thrill of running a business still looms? He notes that eventually, that day comes, and transitioning power is a delicate process, especially when you consider your legacy, tax concerns, heirs (whether or not they are taking over the business) and dozens of other often forgotten about aspects.

John does say that the exiting process, which should be a joyful time, can become burdensome and require professional financial assistance. With that, the group begins to break up, each having gained a bit of clarity in regard to their particular situation.

No matter what cycle they are in, entrepreneurs are a fascinating and admirable breed; however, they don’t know everything. That’s why they sometimes need outside help. The key is recognizing that no two businesses or financial situations are alike and, therefore, can’t be addressed with a rote game plan. No matter what cycle you are in, your situation is unique, even compared to others in the same cycle. If you are a new business owner, seek advice from seasoned veterans, but remember that you are in your own season. If you are the veteran offering advice, take into account how the industry has changed since you were starting out. After all, we know what to plant each spring, but we don’t know what kind of harvest summer will allow.