The vicious job loop is an endless cycle of misrepresentations and mistruths. There are so many things that can go wrong in job cost reporting and the interesting thing is that most of the issues lie not in information technology but with human psychology. Sure, there was a time when there was not a great, seamless system of real time feedback, allowing construction organizations to make project course corrections.

However, most systems on the market today provide timely data, allowing you to make better decisions earlier in any project. If there are adequate systems for just about every type of contractor, why do projects routinely go over budget in most direct cost categories?

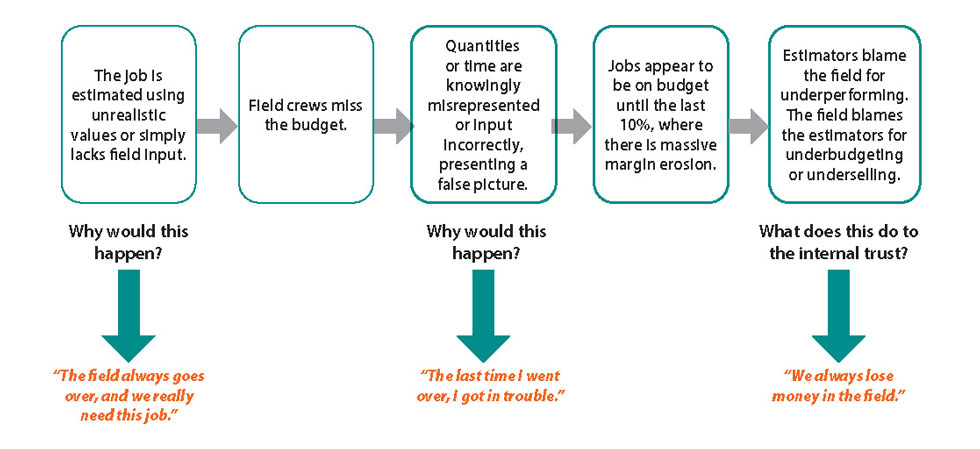

Figure 1 illustrates the common occurrence adversely impacting the job reporting cycle. The most obvious disconnect is the lack of clarity and collaboration that so many organizations fail to capture.

Whether it is an outright snub or simply an oversight, too many organizations bid projects without realistic feedback from the field. The field then proceeds to build with a distrust of “the numbers,” giving little credence to the budget set forth. It isn’t until the end of the project that the score of the game can be actualized and even both the office and field can hardly explain how the proverbial sausage was made.

As an operations leader, it is critically important to examine the root causes of these behaviors to not only leverage their technological platforms but also drive superior operational performance.

Filling the Buckets

Consider a firm with only three cost codes. A drywall contractor with “framing,” “hang drywall” and “finish drywall” codes — or a civil contractor with “clear and grub,” “rough grading” and “finish grading.” Three linear codes that in essence capture the hours associated with each phase of a project — beginning, middle and end. But how often does an organization believe they underperform in that third code when they really operate poorly in the first code?

Examine the root cause — the field leader is overrunning that first code’s labor budget. Rather than run over, time is charged errantly to the second code. Subsequently, the same thing happens again, until that third code is utilized. And since there is no fourth labor code, the end result is a distorted overage. The primary reasons for even considering the initial overrun comes down to misguided optimism, ego and fear. Ego may be tough to predict, but operational leadership cannot exacerbate this problem with chastisement. There is a difference in asking, “Why did we go over?” and asking, “Why did you go over again?”

The overage may have been an estimating error or site condition but if the answer is always viewed as a field problem, the root cause may never appear.

Correcting The Course

Imagine playing a basketball game in which the scoreboard was broken. Two teams play a game without knowing the score. The only feedback they receive is at halftime or at the end of the game.

As farfetched as this sounds, how often does the field receive feedback on their performance? At the end of the project? Much of the software today can provide real time labor feedback yet the field never hears about how a job is performing. If they do hear, it is normally long after corrective action can be made.

The important questions to ponder are as follows:

- Is the forecasting and cost feedback process iterative and collaborative?

- Is there an interactive process that brings the office and field together to review?

- How often does the project team actively manage the costs and bring them into prime focus?

It’s hard to turn a ship that has run aground. In the same way, a project that fails probably had good indicator lights to provide predictivity.

However, if no one is using the data to manage the project or believes the data is inherently in error, there may be more insidious factors at play.

Managing Change Orders

Hearing from a project team, “That code has a change order attached to it.” is a little like hearing, “The check is in the mail.” First, it is hard to gauge performance in the short term if there is an asterisk of a change order buffering realism.

Secondly, how hard is it to trust the information you are seeing if you are the field leader. Am I really behind, or am I ahead? Will I be behind later? There is not an easy solution for a change order manager relative to job cost feedback.

However, consider the following — a few words to the wise:

- If this is truly a change order — one that is either expected or possibly subject to debate — inform the field that they are to charge time to a different code altogether.

- Additionally, even if the change order is under debate or contention, adjust the budget.

While this sounds like heresy, if the organization has committed to doing the work — without an approved change order — there is a budget. Collections are a different thing entirely and while there may be no applicable revenue to offset, the field needs to see realism in production rates and budgets.

A business decision to proceed with work on a change order that may make the firm zero profit should not distort the field’s production budget. Lastly, one solution would be timely processing and collection of all change orders.

Recognizing Behaviors

Job cost feedback should be timely, realistic, collaborative and functional. The tools are available to do this correctly. The scoreboards are fully operational, and it is it important to recognize the most likely impediments to accuracy and timeliness are rooted in bad behaviors.