Editor’s Note: This is the first in a six-part series titled “The Project Manager’s MBA,” which analyzes six key components of leading business practice and applies them to the construction industry.

Managers and executives of every facet of business have embraced the Master of Business Administration, or MBA, as the pinnacle of business education. From Harvard to Berkeley, Wharton to Fuqua, these programs emphasize accounting, finance, marketing and managerial principles through painstakingly detailed case studies and laborious research projects.

With complicated projects draped in risk and executed by firms barely liquid enough to make weekly payroll, construction businesses arguably stand the most to gain from the nation’s greatest business curriculum. However, construction business leaders largely fail to capitalize on this knowledge. Absorbed in traditions and beliefs of past generations, many construction firms putter along while other industries leverage new concepts, technologies and models to grow.

To be successful, construction businesses cannot focus only on being great builders; they must invest in establishing themselves as business enterprises. In order to build such a legacy, construction business managers and owners should have at least a basic understanding of the core components of the nation’s greatest MBA programs:

• Finance and accounting

• Economics

• Organizational behavior

• Marketing

• Ethics

• Operations management

This six-part series, “The Project Manager’s MBA,” will begin with the first of these topics: finance and accounting.

Finance and Accounting 101

Many business discussions revolve around the concept of cash flow. Collecting receivables has long been viewed as an accounting function and a distraction to the process of building, but more progressive contractors have noticed that those with the most intimate knowledge of projects—and of potential obstacles to getting paid—were previously not involved in the process. Since then, the marriage of management and finance has become a cornerstone of project management.

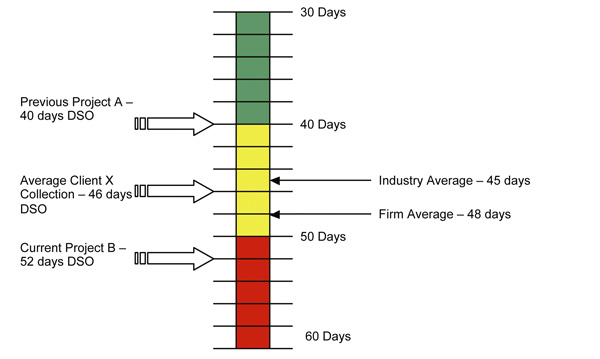

Collections

Forty-five days. Sixty days. Ninety days. Days sales outstanding figures continue to creep into contractors’ financial danger zones. Contractors and suppliers often essentially provide interest-free financing for large projects under construction. To them, collecting the money is secondary to completing the project.

The first challenge to overcome is the stigma of focusing on receivables rather than the construction process. In a low-margin industry such as construction, cash flow is critical—especially considering that contractors often carry the bulk of the risk. Managers must find a mechanism to evaluate their projects’ cash-collection performance.

The first challenge to overcome is the stigma of focusing on receivables rather than the construction process. In a low-margin industry such as construction, cash flow is critical—especially considering that contractors often carry the bulk of the risk. Managers must find a mechanism to evaluate their projects’ cash-collection performance.

Industry-wide, there is a sense of complacency regarding cash collection. Most firms neither adjust pricing nor consider the time value of money when dealing with customers known to be late payers. Some argue that doing so would make them less competitive. If that were the case, wouldn’t a proactive collecting strategy prove more effective? Poorly performing contractors bid from the gut, failing to understand the power of collections. Best-of-class firms utilize benchmarks and approach their transactions with the sophistication of a businessperson.

Margin Contribution

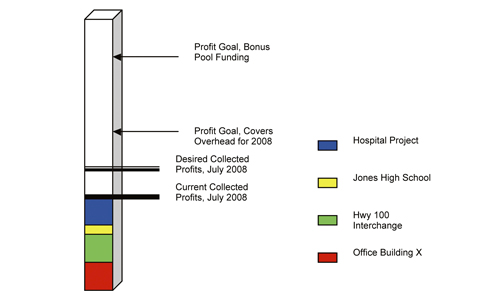

Philanthropic organizations around the country provide one of the greatest types of visuals for illustrating margin contributions. Gigantic thermostats adorn the landscape of churches and charities, using the rising mercury to signify contribution collections. Corporate leaders would benefit from using the same technique to represent the contribution of projects to the bottom line on a monthly basis. Figure 2 is an example of a margin contribution chart that could be utilized by a construction firm to illustrate projects’ influences on income.

Razor-thin margins in the construction industry are no secret. However, studies have shown that the further an employee is from the office, the more the perception of profitability becomes inflated. Thus, those who are closest to the project and who wield the greatest influence on profit capabilities have the most misguided notions about margin contributions. Educating employees about a company’s margins with accessible depictions of income will allow them to understand the degree to which projects contribute not only to the organization’s goals but also to the goals of the employees themselves.

Razor-thin margins in the construction industry are no secret. However, studies have shown that the further an employee is from the office, the more the perception of profitability becomes inflated. Thus, those who are closest to the project and who wield the greatest influence on profit capabilities have the most misguided notions about margin contributions. Educating employees about a company’s margins with accessible depictions of income will allow them to understand the degree to which projects contribute not only to the organization’s goals but also to the goals of the employees themselves.

It is common to have both project gains and project losses. However, even controllable losses tend to be regarded as “the cost of doing business.” Superior project managers understand the full value contained in any loss and the importance of controlling these losses.

The concept of margin contribution is not complicated. Those who focus on the bottom line from beginning to end have the ability to create margin gain.

Purchasing Strategy

Purchasing materials and subcontractors is one of the most integral managerial processes in the supply chain of a construction business. Often, purchasing is done more as an exercise to keep the project moving rather than a strategic move to gain additional margin, and to many contractors, efficient purchasing is defined as how far a supplier and subcontractor can be “beat down” on price. For some, the fine line between ethics and effective management becomes blurred in a process known as “bid shopping.”

A clear and definitive process used to gain margin within the boundaries of sound business sense should include the following:

Hedging – Should purchases be strategically accelerated, delayed or staggered to achieve margin gains in price fluctuations?

Bulk Purchasing – Should purchases be made in bulk with other projects to receive discounts?

Purchasing Matrix – Using a series of pre-qualified vendors and contractors, a matrix should be used to analyze additions, alternates, qualifications and exclusions.

Purchasing Goals – Management should aim to purchase all materials within a certain percentage of the project schedule, with the exception of those earmarked as strategic purchases. For example, management may mandate that all purchases be made within the first 15 percent of the schedule.

Material Handling – Each component should be examined to reduce transportation costs to the office and to the project site. Furthermore, careful consideration should be given to how the material will be placed onsite to reduce labor-handling costs.

Purchasing Terms – All purchasing terms should be carefully reviewed, and an analysis of cost savings should be conducted. If paying in two weeks for the life of the project saves $20,000 and the project can remain overbilled, the decision should be easy, even if it breaks with protocol.

Smart and ethical purchasing sets the tone for a project. Using these financial instruments to achieve a deeper understanding of the dollars behind a bid separates managers from purchasers.