It is apparent that lean and fit organizations represent a platform for long-term survival. With the challenges of the current economic times, contractors are leaving no stones unturned.

They have recognized the importance of imagination, vision and competitive information to survive and succeed in an uncertain world. In this respect, risk management has emerged as an important source of creativity and vision that is enhancing the competitive edge and, in some cases, the survival rate of many contractors. Managing risk has been transformed from a once-a-year insurance bidding frenzy to a serious management initiative that has the ability to boost returns, create equity, reduce costs and permanently change the way construction firms are managed.

The risk management technology available today has long passed the traditional construction risk insurance policy buyer in favor of sophisticated construction firms that are astute enough to put each and every risk dollar to work for the company, stabilizing and reducing cost while leveling out the losses. The following represents a few selected risk management technologies that contractors are embracing to weather the storm.

Contract Documents

Allocating risk on construction projects continues to be an often-overlooked area in analyzing risk profiles for contractors. The effective use of hold harmless and indemnification agreements can reduce, and oftentimes manage, specific types of losses (particularly "action-over" lawsuits) that would have been otherwise absorbed into the contractor's operations or insurance program. To capitalize on this technology:

- A standard subcontract document and purchase order should be reviewed for enforceability within the state venues of work and updated periodically to incorporate state laws. Whatever form is chosen, this agreement should serve as the basis for distributing risk within projects.

- This standard subcontract/purchase order should contain specific language with respect to types of policies/coverages required, minimum limits of liability and endorsements that protect the interest of the construction entity seeking indemnity. For example:

- Additional Insured-adding the name of the general contractor to a subcontractor's general liability policy as an additional insured. Due to the new proprietary forms being used by insurers, this is becoming a challenging issue with regard to completed operations, ongoing operations, residential restrictions and indemnity agreements. There are countless forms being used, with many having significant restrictions on additional insured benefits/status. To date, we have identified fifteen serious restrictions or exclusions contained in many of the forms with the intent to restrict or even withdraw additional insured benefits to the contractor.

- Insurance Considered Primary-the liability program of the subcontractor or sub-subcontractor shall be considered primary in the event of a loss.

- Cancellation Notice-usually as much as sixty days for cancellation and/or non-renewal is desired.

- Waiver of Subrogation-to avoid subrogation proceedings on losses by the subcontractor's insurer.

- As a rule, coverages should include general liability, automobile liability, worker's compensation, umbrella and certain types of property policies, such as builder's risk/installation floater for work to be installed or erected. Coverage areas need to be quite specific and include limits, endorsement language and specific reference to the indemnification agreement signed by the parties. Additional coverages, such as professional liability or pollution liability, should be carefully examined, depending upon the project scope.

- Each project file should contain a standard certificate of insurance specifying coverages and limits and should include actual additional insured endorsements. All coverages, particularly liability, should be maintained throughout the project and continued for a given period of time (typically two to five years) after completion.

- An audit of the certificate process should be conducted annually on major projects and on subcontractors to verify that the administration of the contract area is being monitored properly.

- A contract checklist should be drafted for review between the contractor and the owner of the project noting specific areas such as limits required and special coverages (e.g., Owner's/Contractor's Protective, Railroad Protective). This checklist can be given to the project bid team for cost analysis, and should include specific owner project financing information to avoid payment pitfalls due to owner budgets or bank financing.

Rating Plans

The insurance marketplace for contractors remains in a bit of transition, with some improvements during the past year. Remaining a competitive, yet profitable, force in the market requires contractors to examine how they are financing losses, such as worker's compensation, liability or auto. With an interest in wrestling redundancies out of every dollar, contractors are embracing more effective methods of procuring insurance and risk management services.

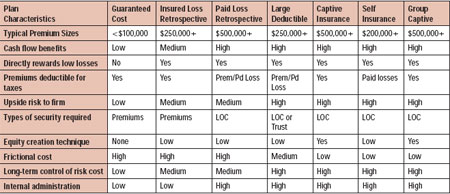

Figure 1 shows the various types of rating plans available for financing a portion of a contracting organization's losses. It's important to match the risk-financing plan with your company's goals, objectives, financial capabilities and cash flow needs. Not all financing plans are created equal-each has its own uniqueness in satisfying a contractor's risk management goals. Choosing the right program is step one. The key to this decision is to compare the program cost of risk thoroughly and completely. A few hints:

- Always analyze the cost of risk on a net present value basis, taking into consideration taxes and the effect that certain rating plans, such as self-insurance, might have on deductibility of premiums or loss reserves.

- Evaluate the cost of funds and your company's internal rates of return for retaining certain levels of risk dollars in-house.

- Look beyond the first year and obtain commitments, or at least an understanding, from the insurance company on how future premiums will be determined, focusing equally on the long-term and the short-term aspects.

- Develop an understanding of the method used by the insurance company in calculating projected losses.

- Match specific and aggregate loss retentions to the company's financial ability to assume losses, either through formal or informal funding.

Despite a more receptive insurance market cycle, contractors continue to retain significant dollars in the form of deductibles, retro limits and aggregate exposures in their operations. In most cases, they are convinced that their ability to prevent and control losses, as well as fund for losses, is far more economically rewarding than simply delegating the entire responsibility to an insurance company, which may have a very different agenda.

Figure 1-Rating Plans for Contractors

Safety Management

Foregoing risk management practices, especially safety management, because of the availability of lower-cost insurance places the contractor at risk in areas not traditionally recognized or even insured. The insurance industry has never drafted a policy that insures every type of risk faced by a contractor. In this vein, risk management, including safety management, is not divisible from effective general management practices.

Best-of-class construction firms usually have an effective safety management program. Effective management and leadership techniques are what really integrate risk and safety issues into a contractor's overall operations. Performance benchmarking areas generally reveal that contractors with above-average net earnings have strong leadership skills. They typically embrace strategic planning seriously, market themselves effectively and integrate risk management into the operations of the firm.

Zero-injury philosophy is directly related to sustainable and profitable construction operations. This is a cultural and philosophical issue that cannot be delegated to a safety engineer from an insurance company or service provider. It's an internal challenge and needs to be driven from within. It all starts at the top of the organization.

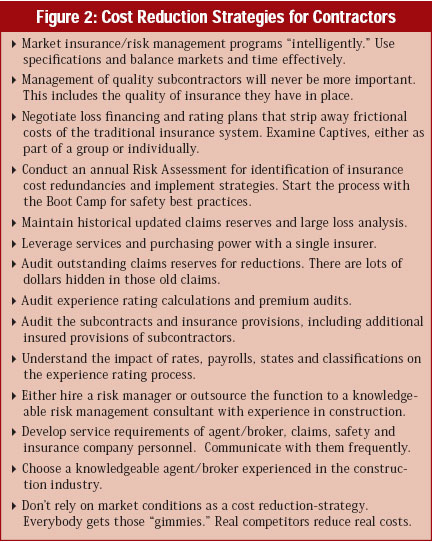

Figure 2-Cost Reduction Strategies for Contractors

The following represent key management practices for safety management that have been identified by several construction organizations for effectiveness in zero-injury technologies:

- Adopt the mental game of zero injury technology. This starts with the chairman of the firm.

- Create an environment of ownership and empowerment among the workforce. This starts with the Safety Management Boot Camp.

- Sell the idea that injuries are not acceptable. Leadership in this area is about getting the workforce to join the effort, not simply following the effort.

- Understand that profits lost through worker's compensation or general liability claims are not covered by an insurance policy.

- Recognize that quality of effort is more important than time spent as zero-injury techniques are implemented throughout the construction process.

- Involve owners and subcontractors as active participants in achieving zero-injury technology. This includes contract documents, risk allocation and methods of insurance transfer used on projects.

Lastly, knowledge continues to be our most important asset, creating the basis of value, revenue and profit. With the supply of information available to us doubling every five years, risk management is maturing into a knowledge-based competitive tool. It's about information, breaking new ground, leaving behind outdated tools for new challenges, taking control while reaping the benefits of the system and the market conditions. Risk management is about creating new ideas to solve new problems.

"The road of adventure leads to wisdom."

Construction Business Owner, April 2010