A common barometer to gauge the state of the economy, construction spending and its growth is the evaluation of a number of key economic indicators, such as unemployment, interest rates and the purchase of durable goods.

Since the burst of the housing bubble, followed by the credit crisis and subsequent Great Recession of 2007-2009, the U.S. economy’s recovery has been tepid.

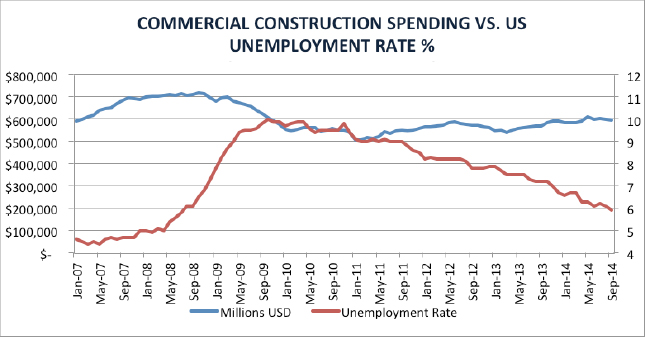

Construction spending figures reinforce the general perception of a slow U.S. economic recovery and an apprehensive approach to investment in commercial construction.

Total construction spending is expected to have grown 7 percent in 2014 and will grow 8 percent in 2015 between the sector’s two segments: private and public. Opportunities are available in private commercial construction, with the strongest growth stemming from office and hotel investment.

Negative growth was observed the first half of 2014 in public construction (minus 0.63 percent in 2014’s first half), with notable contraction in public safety (minus 4 percent forecast for 2014) as federal budgets remain cash-strapped. Although challenged, public spending is expected to turn positive by the end of 2014.

Commercial Construction Recovery

At the start of 2008, just as the U.S. was in the first months of what came to be known as the Great Recession, total construction spending (public and private) was approximately $1.1 billion (seasonally adjusted annual rate). It declined 30 percent to $760 million by the first quarter of 2011.

Since this low point, total construction spending has increased 25 percent to $951 million as of the third quarter of 2014, rising along with consumer sentiment.

However, as exhibited by the chart in Figure 1, this is still 13 percent below the start of the recession, and this disparity grows more when compared to the height of the construction boom in the mid-2000s when unemployment was 4.5 to 5.5 percent (versus 5.9 percent as of October 2014).

Figure 1 (Source: Euler Hermes North America, Inc., U.S Census Bureau, Bureau of Labor Statistics)

Figure 1 (Source: Euler Hermes North America, Inc., U.S Census Bureau, Bureau of Labor Statistics)When the two major components of construction spending are examined individually, public construction has proven far less volatile since 2008 than private construction spending. This is primarily due to U.S. government stimulus packages distributed throughout the country for various infrastructure projects, effectively shielding a decline. However, this infusion will eventually run its course and, coupled with constrained municipal and state budgets reducing public construction projects, we have seen a slight decline through the third quarter of 2014.

Congress, however, recently extended the current highway bill to May 31, 2015, spurring street and highway spending, and sending a slight jolt into public construction, which is now expected to grow 1 percent in 2014 and 3 percent in 2015.

Private Construction shows Double-Digit Growth

Private construction contributes over 70 percent of total construction spending with expected 10 to 11 percent growth, including home building.

Commercial construction spending overall has experienced growth in the low teens in 2014, with even stronger growth expected in 2015. This growth is primarily driven by office construction, where technology and finance companies have contributed to expansion.

According to Dodge Data & Analytics, commercial starts have also displayed healthy increases in 2014, at 23 percent to $27.1 billion, with a further rise of 19 percent to $32.3 billion expected for 2015.

The cream of the crop throughout 2014, however, has been the manufacturing sector, driven primarily by the oil and gas industry, which increased starts by 57 percent. However, the boom of the past several years is expected to soften, with forecasted growth of just 16 percent to $24.4 billion anticipated for 2015, as companies are cutting spending due to lower crude oil prices.

On the institutional and public works side, moderate growth is expected as well for 2015, at 9 percent and 5 percent respectively. K-12 school construction is aided by greater access to financing as construction bonds have become more generous. Public works experienced a difficult 9 percent decline in 2014, but is expected to rebound due to increased highway and bridge construction.

Overall, after sluggish growth in the past several years, the nonresidential construction industry experienced significant growth in 2014.

Looking forward in 2015, as companies gain confidence, expand operations and lease additional office space, tremendous opportunities lie within private commercial construction.

Expectations are for growth in office and hotel investment of approximately 13 to 14 percent because of pent-up demand, as well as manufacturing facilities to support the chemical and tire industries, which are bringing back investment from overseas as feedstock has become cheaper given the U.S. shale oil boom.